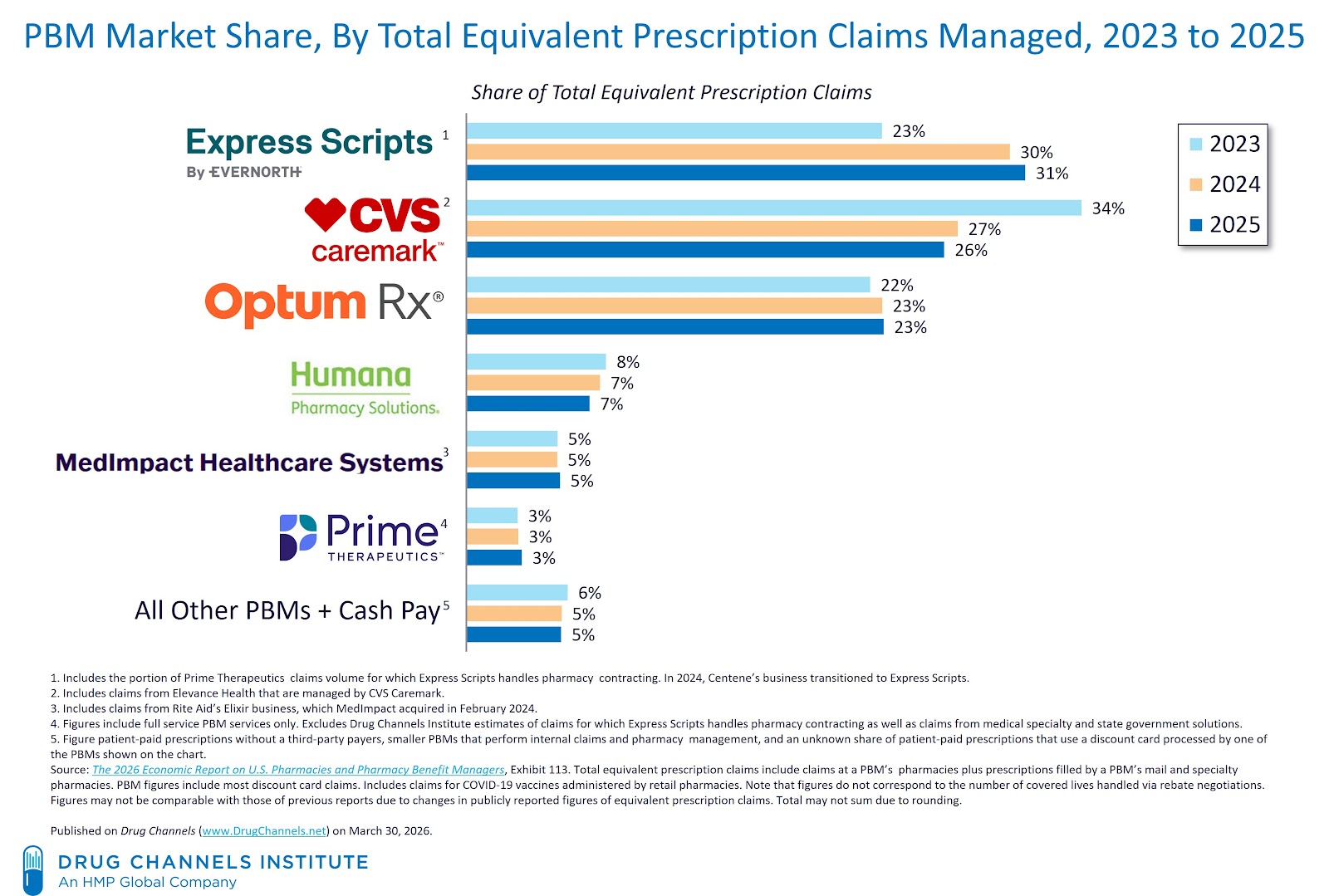

Three is still the magic number for pharmacy benefit managers (PBMs).

By 2025, 80% of all prescription claims will be processed by three companies: CVS Health’s CVS Caremark business, Cigna’s Express Scripts business, and UnitedHealth Group’s Optum Rx business. Express Scripts continued to pull ahead of its peers, while CVS Caremark’s claim volume declined for a second straight year.

Independent PBMs continued to receive business from these larger PBMs, showing a erosion in margins. Many smaller PBMs still rely on their larger competitors for claims processing, network management, and waiver negotiations. So even if a plan sponsor chooses an alternative PBM, the Big Three can still win with behind-the-scenes economics.

Below, we highlight the new DCI 2026 Economic Report on US Pharmacies and Pharmacy Benefit Managers To break down the latest market share data for major companies.

The dominance of the Big Three PBMs continues, but they face increasing regulatory and competitive obstacles. The largest PBMs are restructuring their businesses in response to customer demands, legislative changes, and legal pressures. emerging Drug net prices channel These changes will accelerate how PBMs generate profits, create contracts, and justify their role in the drug channel.

PBM Industry Update 2026: Trends, Challenges, and What’s Ahead.

For a deeper dive into the state of the industry, register for DCI’s next webinar on April 10, 2026, from 12:00 pm to 1:30 pm. Adam J. Fein and Bryce Platt will unpack the good, the bad, and the ugly of the PBM industry—and explore what it means for you. Click here to learn more and sign up.

2025 Big PBM Numbers

DCI estimates that by 2025, 80% of all prescription claims will be processed by three companies: CVS Healthcare’s Mark Care business, Cigna’s Express Scripts business, and UnitedHealth Group’s Optum Rx business. This share is consistent with the overall share of large PBMs over the past few years. This level of concentration remains unusually high – and remarkably stable – given the policy and competitive noise surrounding the industry.

Note that the 80% figure refers to prescription claims processed, not the number of covered lives handled through discount negotiations. This distinction is frequently misunderstood, as discount aggregation (discussed below) creates an even larger scale illusion. This data appears in Chapter 5 of our new 2026 Economic Report on US Pharmacies and Pharmacy Benefit Managers.

[Click to Enlarge]

Here are the latest market developments for some major companies:

- Express Scripts (Cigna). The ExpressScripts business is reported in the Evernote Health Services segment in Cigna’s financial reports. Evernorth also operates myMatrixx, a PBM focused on workers’ compensation.

Express Scripts claimed the top spot for the second year in a row. Express Scripts’ total adjusted prescription claims grew 4.8%, from 2.12 billion in 2024 to 2.22 billion in 2025. (See Exhibit 114 in our new Pharmacy/PBM report.) This growth reflects both organic expansion and the continued consolidation of major customer relationships.

The rise to the top of the PBM pile comes from several sources, including:

- Cigna’s PBM business transferred to ExpressScripts from Optum Rx following the Cigna-ExpressScripts combination

- ExpressScripts multifaceted strategic relationship with Prime Therapy, which now relies on ExpressScripts for nearly half of its entire network

- Centenary 2024 Switch from CVS Caremark to Express Scripts

- TRICARE, which in 2024 required beneficiaries to use an Express Scripts accredited specialty pharmacy or military pharmacy to fill prescriptions for certain maintenance drugs.

Express Scripts’ growth and declining customer concentration were evident last year, when Cigna reported profit pressure after “actively improving the economic terms of contracts to benefit its long-term strategic customers.” Translation: Centene and Prime Therapeutics got better deals in return for their volume.

- A CVS Care brand (CVS Health). The PBM business is part of CVS Health’s Health Services segment, which includes CVS Caremark, Cordavis, Oak Street Health, Signify Health, and MinuteClinic.

For 2025, PBM 30-day equivalent claims processed decreased 0.9%, to 1.9 billion. CVS Caremark’s claims volume is expected to reach 2.3 billion in 2023, before Centen’s PBM business is transferred to Express Scripts in January 2024.

For 2026, Caremark should grow as it replaces Optum Rx as the PBM for the California Public Employees’ Retirement System (CalPERS).

CVS Health provided certain PBM services to Elevance Health’s CarelonRx business, including PBM administrative functions such as claims processing and prescription fulfillment services. Behind-the-scenes service relationships further blur the lines between competitors and colleagues. In 2024, the CVS contract was extended for another three years until 2027. Elevance has the option to extend for an additional three years under the same terms and conditions.

- Optum Rx (United Health Group). UnitedHealth Group became the third largest PBM when it began using its internal Optum Rx PBM subsidiary for its commercial PBM business.

For 2025, it managed $188 billion in drug spending, of which $87 billion (46%) was classified as specialty drugs by Optum Rx. Optum Rx equivalent claims grew by 36 million (+2.2%), from 1.623 billion in 2024 to 1.659 billion in 2025.

Optum Rx’s largest customer is UnitedHealthcare, the health insurance business of UnitedHealth Group. For 2025, UnitedHealth Group’s internal business will account for 63% of Optum Rx’s revenue. This is a structural advantage that allows Optum Rx to maintain its position in a way that competitors cannot easily replicate. The remainder comes from unbundled commercial health plans, employers, and Medicaid programs.

- First treatment. Prime serves as the PBM for 23 Blue Cross and Blue Shield health plans and those plans’ subsidiaries and affiliates. Nine of these plans are collectively owned by businesses. Prime also provides PBM services to more than two million lives through non-blue collar health plans and self-funded employer groups.

For 2025, Prime reported $55.3 billion in prescription spending and 407 million claims, compared to $52.7 billion in spending and 411 million claims in 2024. These figures include only full-service PBM services and exclude claims from Medical Specialty and State Government Solutions. Because of Prem’s relationship with Express Scripts, about half of her version claims include the Express Scripts figures shown above.

In 2022, Prime Therapeutics completed the acquisition of Magellan Rx from Centene. In 2024, Prime Therapeutics invested $115 million in JUDI Health (then known as Capital Rx) and announced an agreement to use JUDI as a trial platform.

In 2020, Express Scripts took over the retail pharmacy network contract for a portion of the Prime Therapeutics business. Prime acquired Magellan Rx in 2022, so ExpressScript’s network claims grew even more as the business moved through 2023. By 2024, we estimate that Express Scripts will handle pharmacy network contracts for about half of Prime’s total network. Consequently, we include these claims in the figures shown above.

For more details on other PBMs, see Chapter 5 of our new Pharmacy/PBM report:

- Section 5.2.2. Provides more details on the Big Three PBMs as well as information on Centene Pharmacy Services, Elevance Health’s CarelonRx business, Humana, and MedImpact Healthcare Systems.

- Section 5.2.3. 18 profiles small PBMs that are privately owned independent businesses or owned retail chains and health systems.

- Section 5.2.4. Examines PBM-affiliated group purchasing organizations.

- Section 5.2.5. Reviews private label businesses that are subsidiaries of the same parent companies that operate the biggest three PBMs.

Behind the numbers

There are several important considerations when reviewing the above figures:

- Collection of discounts. The figures above do this no Corresponds to the number of covered lives governed by the discount negotiation.

Many small PBMs do not have the scale to communicate reasonable formulary discounts and may not have a claims processing system in place. In these cases, a large PBM acts as an aggregator for these smaller entities. Larger PBMs offer a larger consolidated invoice, and smaller players get better pricing and access to a national claims system.

Rebate collection also occurs through large PBMs’ group purchasing organizations, which manage rebate negotiations with manufacturers and provide other services to manufacturers and group members. Until now, these groups have focused on commercial, non-governmental businesses. The three major purchasing groups owned by PBMs are:

- Ascent Health Solutions, which is jointly owned by Cigna Spruce Holdings GmbH (a wholly owned subsidiary of Cigna), Kroger, and Prime Therapeutics.

- Emissar Pharma Services, part of UnitedHealth Group’s flagship business.

- Zinc Health Services, a US-based contracting entity, was created by CVS Health. Elevance Health reportedly has a minority interest in Zinc.

There are also smaller PBM-dependent GPOs.

We describe these GPOs in Section 5.2.4. Our new pharmacy/PBM report.

Because of this sum, there is significant double counting when evaluating covered life. Summarizing the data reported by individual PBMs results in a total number of lives greater than the total population of the United States.

- Claims processing and pharmacy network management. The large companies’ figures include an unknown number of claims from smaller PBMs. This is because many small PBMs claim processing and fulfillment to one of the three largest PBMs. Smaller PBMs with internal capabilities are included in the “all other PBMs” category.

- Discount cards and cash payment versions. Prescriptions paid by a patient using a discount card are not considered cash, as claims are adjudicated by the PBM. A growing (but unknown) share of discount card claims is included in the figures for each PBM.

We save the term Cash payment version For claims that are not submitted and adjudicated, the PBM or third-party payer does not have a record of drug use. Instead, the patient is the payer and there is no PBM involvement.

#Top #Pharmacy #Benefit #Managers #Market #Share #Key #Industry #Developments